What's a Good Allowance for a Kid? 2026 Guide

TL;DR:

- A suitable allowance for a child is about one dollar per year of age per week, adjusted for family budget and expenses. Regular money conversations and structured practices like the give, save, spend model teach real financial skills better than the amount itself.

A good allowance for a kid is an age-appropriate weekly amount that teaches financial responsibility, commonly around $1 per year of their age. So a 7-year-old gets $7 per week, a 10-year-old gets $10, and so on. This guideline, widely known as the dollar-per-year rule, is a starting point, not a fixed rule. The best allowance amount for kids depends on your family budget, what expenses the money is meant to cover, and your child’s ability to understand money. The goal is never just to hand over cash. It is to build real financial habits that stick.

What’s a good allowance for a kid by age?

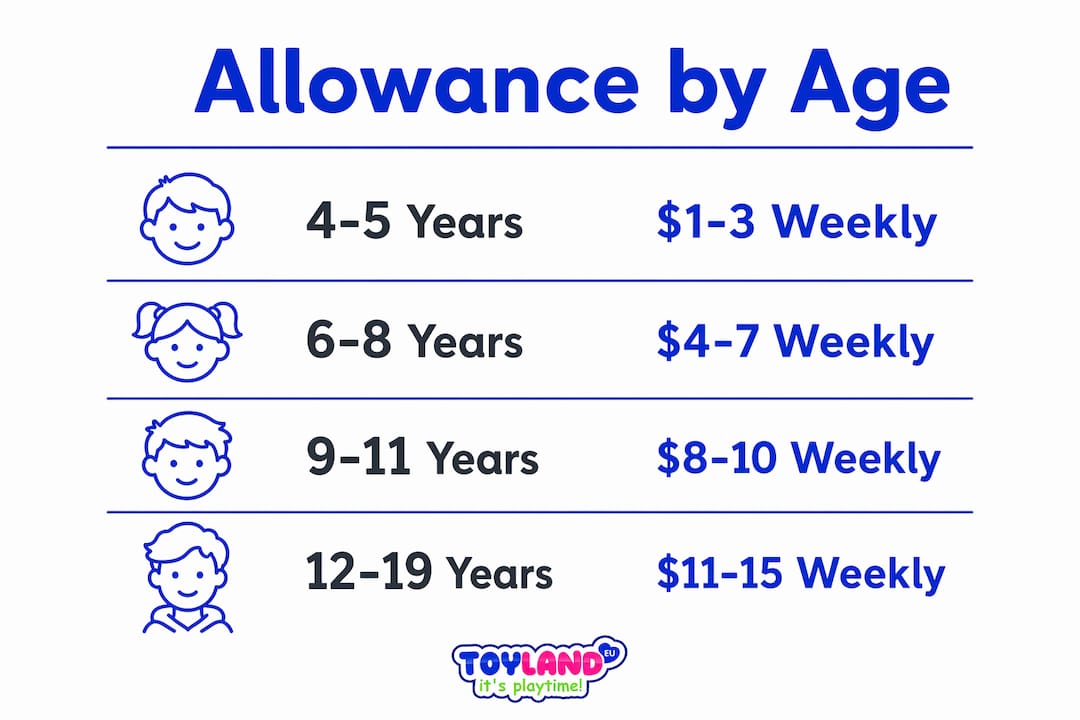

The dollar-per-year rule is the most widely adopted guideline for setting a child’s allowance. It suggests ages 4–5 receive $1–$3 per week, while teenagers aged 15–17 receive $15–$25 per week. That range reflects the growing cost of a teen’s social life, school needs, and personal spending.

Real-world data backs this up. The average weekly allowance for kids aged 5–19 was $13.15 as of 2025, scaling from about $6.18 at age 5 to $21.47 at age 17. That gap shows how much a child’s financial needs grow over just a decade.

| Age group | Typical weekly allowance | Common spending categories |

|---|---|---|

| 4–5 years | $1–$3 | Small treats, stickers, simple toys |

| 6–8 years | $4–$7 | Books, small games, snacks |

| 9–11 years | $8–$10 | Apps, outings, hobby supplies |

| 12–14 years | $10–$15 | Clothing extras, entertainment, gifts |

| 15–17 years | $15–$25 | Dining out, clothing, digital subscriptions |

Younger children in the 5–8 age range average about $6.66 per week. Kids aged 9–11 average $8.58 per week. Teens aged 12 and up average $18.11 per week. These figures reflect real spending patterns, not just theory.

Most experts recommend starting allowance at age 4 or 5, when children can begin to grasp the concept of money value. Younger children respond better to non-monetary rewards like stickers or privilege points.

How to decide the best allowance amount for your child

The right amount is the one your family can pay consistently. Consistency matters more than size. A child who receives $5 every Friday learns more than one who gets $20 unpredictably.

Start by deciding what the allowance is supposed to cover. That decision changes the number significantly.

- Basic spending money only: Stick close to the dollar-per-year rule.

- Snacks and school extras: Add $2–$5 per week to cover those costs.

- Clothing and apps: Teens covering their own clothing or digital subscriptions need $15–$25 per week or more.

- Social outings: Factor in local costs. A movie ticket and snack can run $20 alone.

Parents should also adjust for family budget and regional cost of living. The dollar-per-year rule was designed as a flexible guideline, not a national standard. A family in a high-cost city may need to scale up. A family on a tight budget can scale down without guilt, as long as the amount stays consistent and the money conversations keep happening.

Pro Tip: Write down a short list of what your child’s allowance is and is not meant to cover before you set the amount. That list becomes your reference point when your child asks for more.

Clear “money responsibilities” prevent arguments. When your child knows their allowance covers snacks but not video games, they learn to plan. That planning is the whole point of the exercise. You can also read more about setting expectations with allowance before you start.

Effective allowance strategies to teach money management

The amount you give matters less than how you structure it. These four practices turn a weekly handout into a genuine financial education.

-

Use the give, save, spend model. Split every allowance payment into three buckets. Typical distribution is 50–60% for spending, 30–40% for saving, and 10% for giving. This teaches budgeting and generosity at the same time.

-

Keep allowance separate from chores. Chores are family obligations, not paid work. Allowance teaches money management, not labor. Mixing the two sends the wrong message: that helping at home is optional if they skip the paycheck.

-

Match payment frequency to age. 61% of parents give allowance weekly, which works well for younger kids who need frequent reinforcement. For teens, biweekly or monthly payments simulate adult financial rhythms and require longer-term planning.

-

Track spending together. Sit down once a week or once a month and review where the money went. This turns abstract numbers into real decisions. A child who sees they spent $12 on snacks in one week starts making different choices.

Pro Tip: Give physical cash to children under 10. Holding real bills and coins makes money feel tangible. Digital transfers work better for teens who already use apps.

Financial conversations are the real product here. The dollar amount is just the entry point. Toys that reinforce learning can extend those conversations into play, which is where young children absorb lessons most naturally.

Common mistakes parents make with allowances

Most allowance systems fail not because of the amount but because of how they are run. These are the four most common pitfalls.

-

Tying allowance directly to chores. When kids earn money only by completing tasks, they learn to negotiate rather than contribute. Chores should be a baseline family expectation. Allowance is a financial education tool, not a wage.

-

Inconsistent payments. Skipping a week or changing the amount without explanation teaches kids that money is unpredictable. That lesson works against everything you are trying to build.

-

Skipping the money talk. Handing over cash without discussion is the most common mistake. Small regular amounts with ongoing dialogue teach saving, spending, and patience far better than larger amounts given in silence.

-

Ignoring developmental readiness. Starting too early, before age 4 or 5, means the child cannot yet connect the money to its value. Starting too late, at 10 or 11, means years of missed practice. Age-appropriate allowance works because it matches the child’s cognitive stage.

Key Takeaways

A consistent, age-appropriate allowance paired with regular money conversations is the most effective way to teach children real financial skills.

| Point | Details |

|---|---|

| Use the dollar-per-year rule | Start with $1 per year of age per week and adjust for expenses and family budget. |

| Match amount to responsibilities | Decide what the allowance covers before setting the number to avoid confusion. |

| Separate allowance from chores | Chores are family duties; allowance is financial education. Keep them apart. |

| Use the give, save, spend model | Split payments into 50–60% spending, 30–40% saving, and 10% giving. |

| Talk about money regularly | Consistent conversations matter more than the dollar amount you choose. |

Why the amount matters less than you think

I have adjusted my kids’ allowances more times than I can count, and the number was never the hard part. The hard part was the conversation that came after. When my oldest was 9, I bumped her weekly amount from $8 to $10 because she started covering her own school snacks. She did not spend the extra $2 on snacks. She saved it. That surprised me. What changed was not the money. It was that we talked about why the amount changed and what it was for.

The parents I see struggle most are the ones who set an amount and disappear. They think the allowance does the teaching on its own. It does not. The money is just a prop. The lesson lives in the conversation about what to do with it. If your budget is tight, start with $3 a week and talk about it every Friday. That beats $20 handed over in silence every time.

Flexibility matters too. A good allowance system grows with your child. What works at 6 does not work at 14. Revisit the amount every year, ideally around a birthday, and treat it as a chance to talk about how their needs and responsibilities have changed.

— Thane Holland

Toylandeu™ has toys that make money lessons stick

Teaching kids about money works best when it connects to something they care about. A child saving up for a specific toy learns goal-setting, delayed gratification, and the real weight of a dollar, all at once.

Toylandeu™ carries over 30,000 toys across every age group, from Montessori drawing kits that support creative learning to RC stunt cars that make a perfect savings goal for older kids. Free worldwide shipping means the price your child sees is the price they save toward. Browse the full catalog at Toylandeu™ and let your child pick their next savings target.

FAQ

What is the standard allowance amount for a 10-year-old?

The dollar-per-year rule suggests $10 per week for a 10-year-old. National averages place kids aged 9–11 at about $8.58 per week.

Should I tie my child’s allowance to chores?

No. Chores are family obligations, not paid work. Allowance is a financial education tool and should stay separate from household responsibilities.

When should I start giving my child an allowance?

Most experts recommend starting at age 4 or 5, when children can begin to understand the value of money. Younger children respond better to non-monetary rewards.

How often should I pay my child’s allowance?

Weekly payments work best for younger children. For teens, biweekly or monthly payments build longer-term planning skills and better reflect adult financial patterns.

What is the give, save, spend model?

It is a budgeting method that splits allowance into three parts: 50–60% for spending, 30–40% for saving, and 10% for giving. It teaches budgeting and generosity from an early age.

Recommended reads

- Should kids get an allowance? A parent’s guide — Toylandeu™

- How toys can supercharge learning: 10 evidence-based tips — Toylandeu™

- The smart parent’s guide to buying toy gifts right — Toylandeu™