Should Kids Get an Allowance? A Parent's Guide

TL;DR:

- An allowance teaches children essential money management skills such as budgeting and saving from a young age. A hybrid model of a small base allowance with optional extra tasks is the most effective approach, emphasizing consistency and conversation. Starting between ages 5 and 7, with amounts proportional to age, helps children develop financial responsibility and understanding.

An allowance is a deliberate, regular payment given to children to teach financial literacy and responsible money management from a young age. The question of whether kids should get an allowance is one most parents face by the time their child turns six. The short answer: yes, with the right structure. About 79% of American parents already give their children an allowance, which shows broad acceptance of the practice. The real debate is not whether to give one, but how to do it well.

Quick summary

An allowance teaches children budgeting, saving, and the difference between needs and wants. Experts recommend starting between ages 5–7 using a weekly amount of $0.50–$1.00 per year of age. The hybrid model, a small base allowance plus optional paid tasks, is the most effective structure. Consistency and conversation matter more than the dollar amount.

TL;DR

- Start allowance at ages 5–7

- Use $0.50–$1.00 per year of age per week as a baseline

- Separate family chores from paid tasks

- Let kids experience the consequences of their spending choices

- The lesson is more important than the amount

Table of contents

- What are the benefits of giving kids an allowance?

- Should allowance be tied to chores or given unconditionally?

- When and how much allowance should kids get?

- How to use allowance effectively to teach money management

- Common pitfalls and myths about kids’ allowances

- Key takeaways

- Perspective

- FAQ

What are the benefits of giving kids an allowance?

An allowance gives children a safe space to practice real financial decisions before the stakes are high. When a child spends their entire weekly allowance on candy and has nothing left for a toy they wanted, that lesson sticks far longer than any lecture about saving.

The core benefits of allowance for children include:

- Budgeting practice: Children learn to divide limited money across multiple wants, which is the foundation of every adult budget.

- Saving habits: Saving for a specific goal, like a LEGO set or a video game, teaches delayed gratification, one of the strongest predictors of financial success.

- Needs vs. wants: Spending their own money forces children to prioritize. A child who blows their allowance quickly learns the difference between what they need and what they simply want.

- Consequence-based learning: Natural consequences of spending teach children more than parental warnings ever will.

- Early financial literacy: 77% of Americans did not understand money until age 18 or later. Starting allowance early closes that gap significantly.

That statistic is striking. It means most adults entered the workforce without basic money skills. An allowance, started young, directly addresses that gap.

Pro Tip: Use the allowance conversation itself as a teaching tool. Ask your child what they plan to do with their money before they spend it. The habit of thinking before spending is the real lesson.

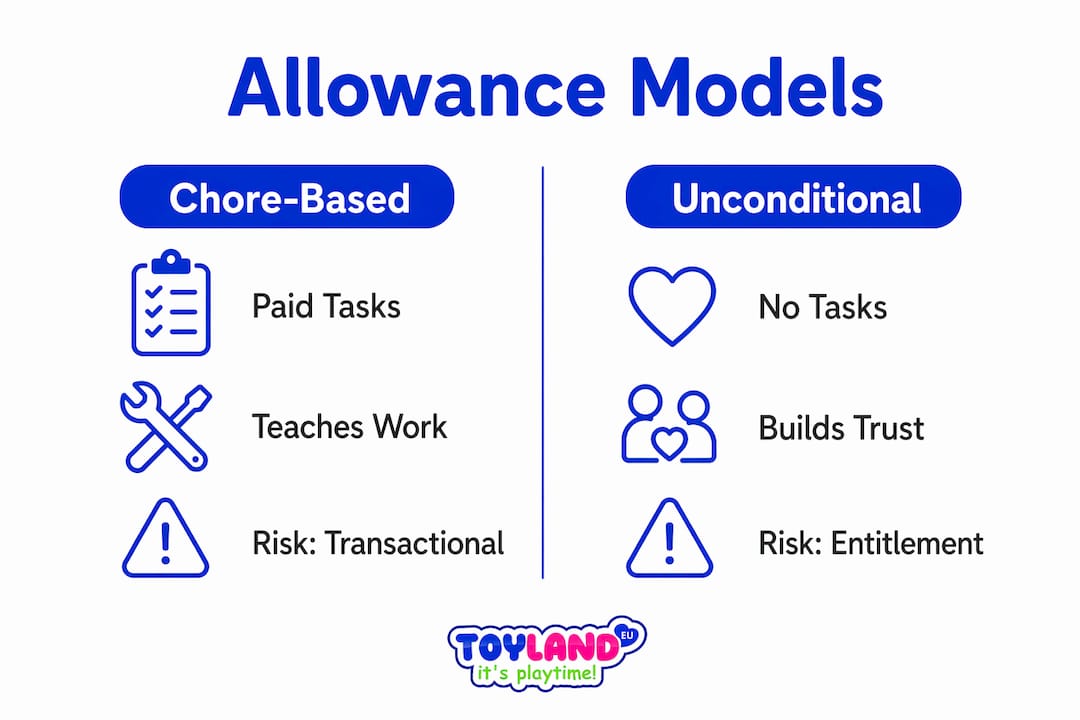

Should allowance be tied to chores or given unconditionally?

This is the most debated question in the allowance conversation, and the answer depends on what you want your child to learn. Each model has real trade-offs.

| Model | How it works | Key benefit | Key risk |

|---|---|---|---|

| Chore-based | Allowance paid only for completed chores | Links work to reward | Kids may refuse chores if they don’t need money |

| Unconditional | Fixed allowance regardless of behavior | Pure money management practice | Misses the work-ethic lesson |

| Hybrid | Small base allowance plus optional paid extras | Balances both lessons | Requires more parental structure |

About 52% of parents tie allowance directly to chores, while 27% use a hybrid model and 20% give it unconditionally. The hybrid approach is the one most financial educators recommend.

Financial authors Ron Lieber and Lewis Mandell both support the hybrid model. Their reasoning is straightforward: the hybrid model preserves family harmony by keeping essential household chores unpaid while creating optional paid tasks for extra income. Dishes and making the bed are family duties. Washing the car or organizing the garage can be paid work.

A pure chore-for-pay system creates a transactional mindset. Children start to see family contribution as optional, something they do only when they want money. That is the opposite of the lesson most parents want to teach.

Pro Tip: List your household chores in two columns: “family duties” (unpaid) and “extra jobs” (paid). Post it on the fridge. This makes the system transparent and removes daily negotiation.

When and how much allowance should kids get?

The right age to start an allowance is generally between 5 and 7 years old. At this stage, most children can count money, understand that it is exchanged for goods, and grasp the basic concept of saving. Starting too early, before age five, usually means the child lacks the cognitive framework to connect money to decisions.

Lemonade Day guidelines recommend a weekly amount of $0.50–$1.00 per year of age. That means a seven-year-old receives $3.50–$7.00 per week, and a twelve-year-old receives $6.00–$12.00 per week. The amount scales with age because older children have more complex financial decisions to practice.

Key principles for setting the amount:

- Match the amount to real decisions. The allowance should be enough to require actual choices, not so much that every want is covered automatically.

- Increase it as they grow. A ten-year-old managing $5 a week learns more than a ten-year-old managing $1 a week.

- Pay on a consistent schedule. Treating allowance like a payday builds the habit of budgeting around a regular income, which mirrors adult financial life.

- Use cash when possible. Physical money creates a tangible experience. Watching coins and bills leave your hand is more emotionally real than a number changing on a screen.

Consistency is the most underrated factor here. A parent who pays late or skips weeks teaches the child that financial planning is unreliable. That is a lesson you do not want to give.

How to use allowance effectively to teach money management

The allowance itself is just the tool. How you structure it determines whether your child actually learns anything useful.

-

Separate family chores from paid tasks. A Cambridge University study found that paying children for every daily chore creates a transactional family attitude and undermines healthy motivation. Keep core duties unpaid.

-

Use the three-jar system. Divide the allowance into three categories: spending, saving, and giving. Physical jars work well for younger children. This is a simplified version of the 50-30-20 budgeting rule adapted for kids.

-

Set a savings goal together. Ask your child what they are saving toward. A concrete goal, like a specific toy or game, makes saving feel purposeful rather than abstract.

-

Let them fail. If your child spends everything on day one and wants money for something on day seven, do not rescue them. Allowing natural consequences is how children build real understanding of needs versus wants.

-

Talk about money openly. The conversation around the allowance matters as much as the money itself. Ask questions: “Was that worth it?” “What would you do differently?” These discussions build financial thinking, not just financial habits.

Pro Tip: Let your child make at least one purchase you privately think is a bad idea. The regret they feel afterward is worth more than any advice you could give.

Common pitfalls and myths about kids’ allowances

Several common mistakes undercut the value of an allowance before it has a chance to work.

- Paying for every chore. This teaches children that family contribution is optional and transactional. Reserve paid tasks for above-and-beyond work only.

- Rescuing children from bad spending. When a child runs out of money, the instinct to help is strong. Resist it. The discomfort of an empty wallet is the lesson.

- Believing allowance is mandatory. An allowance is not the only path to financial literacy. Letting children manage birthday money, participate in grocery budgeting, or control a small gift budget can teach the same skills without a formal weekly payment.

- Focusing on the dollar amount. Parents often stress about whether $5 or $10 is the right number. The amount matters far less than the consistency, the structure, and the conversations that surround it.

The goal is not to give children money. The goal is to give them practice.

Key takeaways

An allowance works best as a structured, consistent practice that prioritizes conversation and real consequences over the dollar amount itself.

| Point | Details |

|---|---|

| Start between ages 5–7 | Children grasp money concepts at this stage, making it the right time to begin. |

| Use the hybrid model | Combine a small base allowance with optional paid tasks to teach both money skills and work ethic. |

| Pay on a consistent schedule | Treat allowance like a payday to build budgeting habits around regular income. |

| Let consequences happen | Avoid rescuing children from spending mistakes so they learn needs versus wants firsthand. |

| The conversation is the lesson | Talking about money decisions matters more than the amount given each week. |

My take after watching kids learn money the hard way

Most parents I talk to overthink the amount and underthink the structure. They spend weeks deciding between $5 and $8 a week, then hand over the money with no system and wonder why nothing changed.

The hybrid model is not just a compromise. It is genuinely the best design for what you are trying to accomplish. It keeps family cooperation intact, creates real earning opportunities, and gives children a money management practice that mirrors adult life. You earn a base income. You can earn more if you take on extra work. That is how the world operates.

The part most parents skip is the conversation. Asking “Was that worth it?” after a purchase is not nagging. It is financial coaching. Children who are asked to reflect on their spending choices develop a habit of thinking before buying, and that habit is worth more than any savings account you could open for them.

I also think parents underestimate how much children want to get this right. When you give a child real money and real responsibility, most of them rise to it. They want to save for something. They want to make a good decision. Your job is to set up the system and then get out of the way.

— Thane Holland

Toys that make money lessons more fun

Teaching kids about money does not have to stop at the allowance conversation. At Toylandeu™, you will find educational toys for children that turn abstract concepts like budgeting, saving, and goal-setting into hands-on play. When a child saves their allowance for weeks to buy something they chose themselves, the toy becomes a trophy for good financial decisions.

The RC gesture-controlled stunt car is a popular savings goal for kids aged 6 and up, and it is exactly the kind of purchase that makes the saving process feel worth it. Toylandeu™ ships worldwide with free delivery, so the reward your child is working toward is always within reach. Browse the full catalog at toylandeu.com and find the toy that becomes your child’s next savings goal.

FAQ

Should kids get an allowance before age 5?

Most experts recommend waiting until ages 5–7, when children can count money and understand basic exchange. Starting before age five usually means the child lacks the cognitive framework to connect money to decisions.

Is allowance tied to chores a good idea?

A pure chore-for-pay model risks making family contribution feel optional. The hybrid model, a small base allowance plus optional paid tasks, is the approach most financial educators recommend.

How much allowance should a 10-year-old get?

A common guideline is $0.50–$1.00 per year of age per week, which puts a ten-year-old at $5.00–$10.00 weekly. The amount should be enough to require real spending decisions.

What if I can’t afford to give an allowance?

An allowance is not mandatory for financial literacy. Letting children manage birthday money or participate in grocery budgeting teaches the same core skills without extra budget strain.

Can trading cards teach kids about money?

Yes. As Next Gen Cards explains, collectible trading cards teach children concepts like value, scarcity, and negotiation, which complement the financial lessons an allowance provides.