Should I Give My Kid an Allowance? A 2026 Guide

TL;DR:

- Parents should give children an allowance to teach budgeting and financial responsibility early. The recommended starting age is around 4 to 5 years old, with amounts scaled to developmental stages. A hybrid model separating core chores from optional paid tasks effectively builds financial literacy without entitlement.

An allowance is a set, regular amount of money parents give their children to practice budgeting, saving, and spending independently. If you’ve been asking yourself should I give my kid an allowance, the short answer is yes. Research shows 79% of American parents already provide one, and the practice correlates with stronger financial literacy. The real question is not whether to start, but how to do it well.

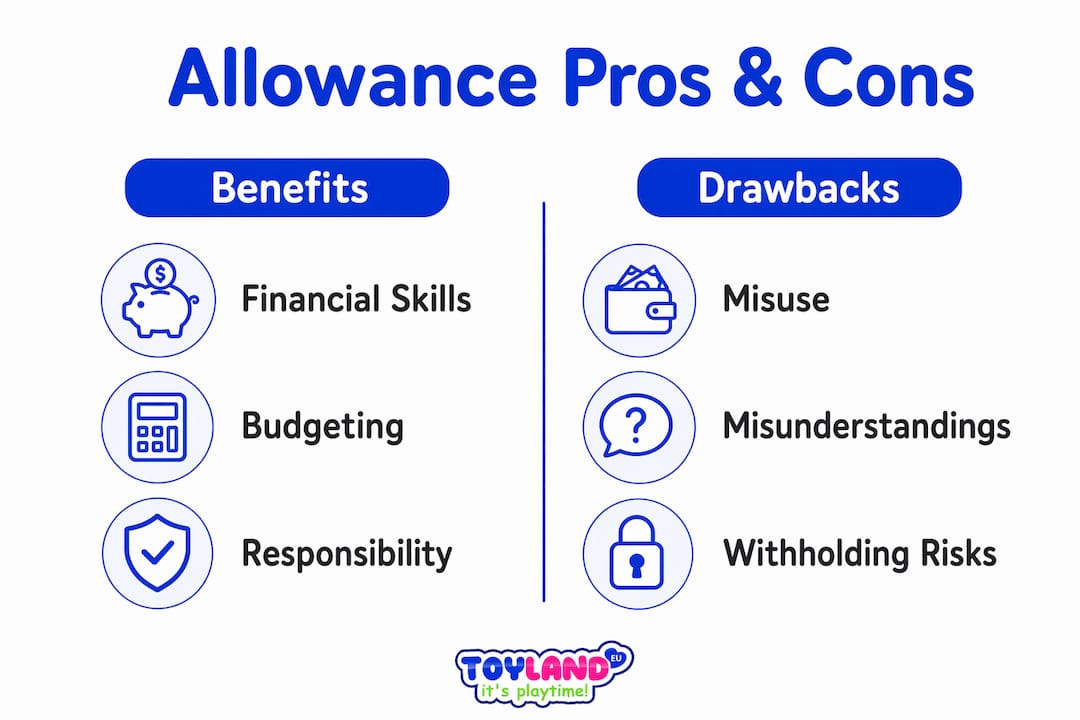

What are the benefits and drawbacks of giving a child an allowance?

Giving kids an allowance builds financial literacy from the ground up. Children who manage their own money learn to make real trade-offs. Spending $8 on a toy today means no money left for something better next week. That lesson sticks far longer than any lecture.

The core benefits of allowance for kids include:

- Teaching budgeting and delayed gratification through real spending decisions

- Normalizing money conversations at home, which reduces financial anxiety later in life

- Building saving habits early, before adult financial pressure arrives

- Giving children a sense of autonomy and responsibility

The risks are real but manageable. 77% of adults reported not fully understanding money until age 18 or later. That gap exists partly because parents wait too long or give money without structure. An allowance without guidance can create entitlement. One with clear rules creates competence.

Pro Tip: Never use allowance as a reward or punishment. Withholding it for bad behavior turns a financial lesson into a disciplinary tool, which confuses the purpose entirely.

When should you start, and how much should you give?

Most child development experts recommend starting around ages 4–5, when children can grasp basic counting and the concept of exchange. Survey data shows 33% of adults prefer starting between ages 8–10, while 22% favor ages 5–7. Both windows work. The key is starting before your child develops spending habits you will have to undo later.

A widely used rule of thumb is $0.50 to $1 per year of age per week. A 7-year-old gets $3.50 to $7 weekly. A 12-year-old gets $6 to $12. This scales naturally with growing expenses and expectations.

National averages in 2026 break down as follows:

| Age range | Typical weekly amount | Primary purpose |

|---|---|---|

| 4–5 years | $1–$3 | Introduce coins, basic counting |

| 6–8 years | $5–$8 | Practice saving and small purchases |

| 9–11 years | $8–$12 | Budget for activities and wants |

| 12–14 years | $10–$20 | Cover personal expenses and saving goals |

| 15–17 years | $15–$25 | Simulate adult budgeting with categories |

Frequency matters as much as amount. Consistent, predictable payments teach children to plan around income cycles. Weekly works best for younger kids. Monthly works better for teenagers, who need to practice stretching money over longer periods.

Should you pay your child for chores or keep them separate?

This is the most debated question in child allowance guidelines, and the answer is nuanced. Tying all allowance to chores creates a negotiation trap. When every household task has a price tag, children start asking “what do I get for this?” before helping with anything. That attitude does not serve them well in families, workplaces, or relationships.

The hybrid allowance model resolves this cleanly. Here is how it works:

- Unpaid core chores: Tasks every family member does because they live in the home. Making beds, clearing dishes, taking out trash. No pay attached.

- Optional paid extra tasks: Jobs beyond normal expectations. Washing the car, cleaning the garage, raking leaves. These earn bonus money.

- Base allowance: Paid regularly, independent of chore completion. This is the financial literacy tool.

This structure teaches two separate lessons simultaneously. Children learn that family participation is not transactional. They also learn that extra effort produces extra income.

Experts consistently warn against using allowance as a bribe or disciplinary measure. When money becomes a behavior management tool, children focus on the transaction rather than the skill.

Pro Tip: Write down which chores are “family contributions” and which are “paid extras.” Post the list somewhere visible. Clarity prevents arguments and keeps the system honest.

How can parents help children manage their allowance well?

The best system for young children is the Save/Spend/Give method. Divide each payment into three physical jars or labeled envelopes. A common split is 50–60% for spending, 30–40% for saving, and 10% for giving. Teens can expand this to include categories like clothing, entertainment, or a personal emergency fund.

Practical strategies that actually work:

- Use physical money for young kids. Coins and bills make abstract concepts concrete. Digital transfers mean nothing to a 6-year-old.

- Set a savings goal together. A specific toy, a game, or a day trip gives saving a purpose. Vague “save for later” advice does not motivate children.

- Open a savings account at ages 10–12. Watching a bank balance grow teaches interest and delayed gratification at the same time.

- Stick to the schedule. Pay on the same day every week or month. Irregular payments undermine the lesson about income predictability.

The most important rule is also the hardest for parents to follow. If a child spends their allowance early, do not bail them out. Let them wait until the next payment. That discomfort is the lesson. Rescuing them removes the consequence and teaches the opposite of financial responsibility.

Pro Tip: When your child wants something they cannot afford, say “How many weeks of saving would that take?” instead of saying no. This shifts the conversation from denial to planning.

Key takeaways

Giving children a regular allowance is one of the most effective tools parents have for building financial literacy before adulthood, provided the system is consistent, age-appropriate, and separated from household chores.

| Point | Details |

|---|---|

| Start early | Ages 4–5 work well for introducing basic money concepts with small amounts. |

| Match amount to age | Use the $0.50–$1 per year of age rule as a starting baseline. |

| Separate chores from allowance | Use the hybrid model: unpaid family tasks plus optional paid extras. |

| Teach the Save/Spend/Give split | Divide each payment into jars or envelopes to build budgeting habits. |

| Never bail out overspenders | Natural consequences teach accountability better than any conversation. |

Why the mindset behind allowance matters more than the dollar amount

I have watched parents agonize over whether to give $5 or $10 a week, and completely miss the point. The amount is almost irrelevant at young ages. What matters is whether money becomes a normal, open topic in your home.

Allowance works best as a communication tool. The weekly handoff is a prompt for a two-minute conversation. “What are you saving for? Did you spend what you planned?” Those questions, repeated over years, build financial instincts that no classroom can replicate.

The biggest mistake I see parents make is starting an allowance system and then going silent about money. They hand over the cash and assume the lesson is happening automatically. It is not. The money is just the prop. The conversation is the actual lesson.

Tailor the system to your family’s values. If generosity matters to you, make the Give jar a real priority and talk about where that money goes. If independence is the goal, let your child make bad spending decisions early, when the stakes are low. A $6 mistake at age 8 is far cheaper than a $6,000 mistake at age 22.

— Thane Holland

Toylandeu™ products that make great allowance spending goals

Children save harder when they have a specific goal in sight. Toylandeu™ offers over 30,000 toys and educational kits that work perfectly as short-term savings targets for kids at every age.

The Montessori Drawing Kit and the colorful drawing scroll kit are both affordable enough for younger children to reach within a few weeks of saving. For older kids, the 24-color clay modeling kit makes a satisfying reward for a month of disciplined saving. Toylandeu™ ships worldwide with free delivery, so the goal stays in reach no matter where you are. Browse the full catalog at toylandeu.com to find the right spending goal for your child’s next saving challenge.

FAQ

Should I give my kid an allowance if they are very young?

Yes. Ages 4–5 are appropriate for introducing small amounts of $1–$3 per week, focused on basic counting and the concept of saving versus spending.

How much allowance should I give my child each week?

The standard guideline is $0.50 to $1 per year of age per week. National averages in 2026 range from $1–$3 weekly for ages 4–5 up to $15–$25 for teenagers.

Is an allowance a good idea if my child already gets everything they want?

Yes, but structure matters more in that case. Set clear limits on what the allowance covers and stop purchasing those items separately. The child needs to experience real trade-offs for the lesson to work.

Should I pay my child for chores?

Core household chores should remain unpaid. The hybrid model separates family responsibilities from optional paid tasks, which avoids entitlement and teaches both cooperation and effort-based income.

What age should I stop giving my child an allowance?

Most families phase out allowance as teenagers take on part-time jobs, typically around ages 15–17. The transition works best when it is gradual, replacing allowance categories with earned income rather than cutting off all support at once.